Why developers raising capital on the Israeli bond market are facing a reckoning — in shekels, in currency, and in court.

Executive Summary

• American developers raised a record $4 billion on the Tel Aviv Stock Exchange (TASE) in 2025 — up 46 percent from the year before.

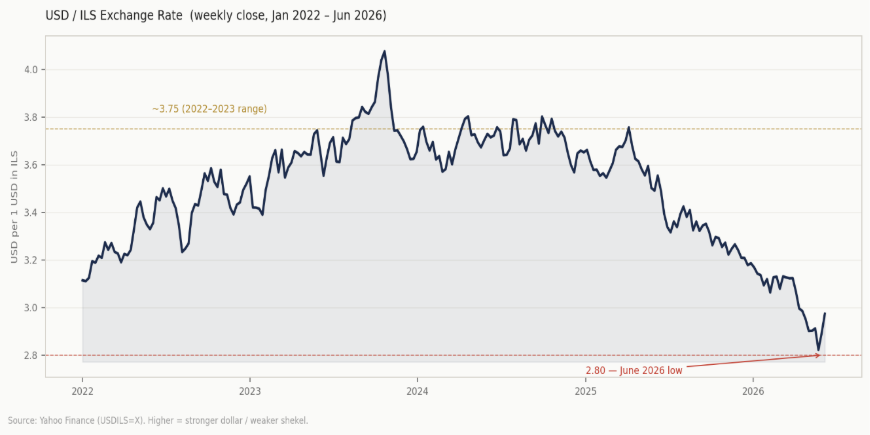

• The shekel has strengthened more than 20 percent against the dollar in the past year, touching 2.80 in early June — its strongest level in roughly 30 years.

• Simad Holdings closed a $195 million TASE deal in December 2025 and filed Chapter 11 in June 2026. Starwood, Hertz, and All Year Holdings had versions of the same problem before them.

• The currency risk, the public disclosure requirements, and the jurisdictional gap in U.S. bankruptcy court were all known risks. Most operators didn’t model them seriously.

In 2015, Stephen Ross’s Related Companies flew to Israel and borrowed $221 million. The rate was better than anything a U.S. bank was offering. The investors were institutional, patient, and hungry for American real estate exposure. Within a few years, dozens of U.S. developers had followed. By 2025, American developers were issuing $4 billion a year in bonds on the Tel Aviv Stock Exchange. Then the dollar started falling — and it didn’t stop. Now one operator is in bankruptcy court, Israeli pension funds are counting losses, and every other U.S. developer with TASE exposure is uneasily reassessing whether this was a good idea after all.

It all traces back to a single policy decision: Israel’s 2008 mandatory pension law, which created a captive and expanding base of institutional capital that needed to be deployed into fixed-income assets. Israeli pension funds, provident funds, and insurance companies were suddenly required to invest, and domestic bond supply was finite. The search for yield pointed outward.

For the first few years the market remained largely quiet — a niche financing option that few U.S. operators took seriously. That changed around 2014, when the first wave of real estate issuers arrived. Related’s $221 million raise in 2015 was the crack that broke the dam. What followed was a flood — dozens of U.S. operators, billions in issuance, and a new line item in the capital stack of American real estate.

By early 2026, the numbers were staggering. Total TASE issuance hit a record $4 billion in 2025 — up 46 percent year-over-year — with 80 to 90 percent of volume coming from real estate firms. More than $20 billion had been raised by over 50 global issuers over the prior decade. Nine new issuers entered in 2025 alone, against a historical pace of one or two per year. (Commercial Observer)

The draw — cheaper capital, longer terms, a funding source entirely outside the U.S. banking system — was hard to resist. The money was flowing, and it seemed nobody wanted to consider the consequences. Consequences that have now become all too real.

Israeli bonds are denominated in New Israeli Shekels, often with CPI indexation layered on top, which means you borrow in shekels but operate in dollars. The shekel has hit its strongest level against the dollar in roughly 30 years, driven by broad global weakness in the greenback. (Jerusalem Post) (Trading Economics)

The U.S. dollar index fell 9.4 percent in 2025 — its worst annual performance since 2017 — and shed another 1.5 percent through early 2026. (NPR) Over the past year, the shekel has appreciated more than 20 percent against the dollar, with the USD/ILS rate falling from around 3.75 to below 3.00 — touching a low of 2.80 in early June.

A developer who borrowed NIS 100 million when the exchange rate was around 3.75 received roughly $26.7 million. At today’s rate near 2.97, that same NIS obligation costs approximately $33.7 million to repay in dollar terms — an increase of $7 million, entirely attributable to currency movement, before a single interest coupon is counted. At the June low of 2.80, that figure climbed toward $35.7 million — a $9 million swing on a single NIS 100 million tranche. For an operator carrying a $200 million bond position, the unhedged FX loss alone can wipe out years of net operating income.

Hedging is the obvious answer. It is also increasingly expensive. As dollar weakness has become a consensus trade, the cost of buying shekel-forward protection has risen materially — narrowing or in some cases eliminating the spread advantage that made the TASE attractive in the first place. The math that made 5 percent Israeli bond rates look better than 8 percent U.S. bank debt looks quite different when you add 200 basis points of annual hedging cost and a structural currency headwind.

That’s before you factor in that roughly $875 billion in U.S. commercial real estate debt is maturing in 2026 — operators already stretched on domestic refinancing are now carrying a shekel obligation on top of it. (Mortgage Bankers Association)

Simad Holdings closed a $195 million bond deal on the TASE in December 2025, backed by summer camps across the Northeast and rated investment-grade by Midroog, Israel’s primary credit rating agency. By late May it had missed its bond payment. By June 4 it was in Chapter 11 in New Jersey. (The Real Deal)

What the collapse revealed had less to do with the specifics of Simad’s business than with how these structures behave under stress. The moment Simad missed its payment, the news was on the Tel Aviv Stock Exchange — public, immediate, and irreversible. There was no quiet call with a lender, no forbearance agreement negotiated over a weekend. The creditor base was thousands of dispersed Israeli retail and institutional investors, and the Israeli financial press was reporting in real time. (Globes)

Then came the jurisdictional tangle. The bondholders believed they held first-lien security on U.S. assets. Those assets sit in U.S. LLCs, inside a U.S. bankruptcy proceeding, in a New Jersey courthouse. The Israeli Securities Agency can regulate disclosure. It cannot compel a U.S. bankruptcy court to prioritize Israeli bondholders. What looked like secured debt is now a claim being sorted out in a jurisdiction that has no particular obligation to Tel Aviv. (The Real Deal)

For the issuer, the experience is its own kind of trap. A U.S. operator in distress would normally work through problems privately with a small group of lenders. On the TASE, that option doesn’t exist. The workout is public, cross-border, and conducted under the scrutiny of a market where reputation travels fast and forgiveness is rare. The door, once closed, tends to stay that way.

Simad is the sharpest recent break, but it is not isolated. Starwood Capital Group surrendered a mall portfolio backing $245 million in Israeli bonds in 2020. (WSJ) Hertz Investment Group (a major national office landlord with no connection to the car rental company) faced a bondholder revolt in 2023 as its U.S. office portfolio deteriorated beneath TASE-raised debt. (CoStar) All Year Holdings, a Brooklyn-based developer, defaulted and restructured more than $560 million in Israeli bonds before entering Chapter 11. Each time, Israeli pension and provident funds absorbed the losses. Each time, the post-mortem pointed to the same structural issues: offshore corporate structures, U.S. bankruptcy jurisdiction, and assets that proved harder to seize than the prospectus implied.

What distinguishes Simad is the speed. Market risk and real estate downturns are priced risks. Israeli institutional investors — who are, ultimately, managing retirement money for Israeli workers — are now asking harder questions about what due diligence they actually received.

For advisors working with clients who have TASE exposure — or are considering it — a few things deserve more scrutiny than they typically get. The currency position needs to be fully stress-tested, not just modeled at current rates. The debt stack needs to account for what happens when a shekel-denominated bullet maturity lands in the same window as a domestic refinancing. The compliance infrastructure — ISA filings, IFRS reporting, FBAR, and FATCA obligations — needs to be treated as an ongoing operational cost, not a one-time closing checklist. And the reputational dimension is real: the Israeli market is small, relationship-driven, and has a long memory. A missed payment doesn’t just close one deal. It closes the market.

The strategy is not dead. Record TASE issuance in 2025 confirms that sophisticated operators and Israeli institutions alike still see a value proposition. But the era of cheap shekel debt with minimal oversight and minimal currency volatility is gone. The shekel has strengthened materially, the defaults have accumulated, and Israeli investors are paying closer attention to the structures they are buying into.

For operators who got in early, executed cleanly, and exited on schedule, the TASE was a genuine competitive advantage. For those still in it — or thinking about getting in now — the entrance may have been inviting, but the exit door is closing.

This material has been prepared for informational purposes only, and is not intended to provide or be relied upon for legal or tax advice. If you have any specific legal or tax questions regarding this content or related issues, please consult with your professional legal or tax advisor.