AHCA Goes to Court

In a May 24, 2024, press release the American Health Care Association (AHCA) announced that, in conjunction with the Texas Health Care Association (THCA) and several Texas long term care facilities, it has filed suit against the U.S. Department of Health and Human Services (HHS) and the Centers for Medicare and Medicaid Services (CMS). In June, trade association LeadingAge, which represents more than 5,400 nonprofit aging service providers, joined the fray and announced that it has joined as co-plaintiff with AHCA. No surprises here. Since CMS’ April 22 release of its final mandate establishing new requirements for nursing homes staffing, healthcare associations and operators have been gearing up for a fight.

“We had hoped it would not come to this; we repeatedly sought to work with the Administration on more productive ways to boost the nursing home workforce,” said Mark Parkinson, President and CEO of AHCA. “We cannot stand idly by when access to care is on the line and federal regulators are overstepping their authority. Hundreds of thousands of seniors could be displaced from their nursing home; someone has to stand up for them, and that’s what we’re here to do,”

AHCA’s complaint argues that the agencies’ decision to adopt the one-size-fits-all minimum staffing standards is “arbitrary, capricious, or otherwise unlawful in violation of the APA.” Further, the lawsuit argues that the rule exceeds CMS’s statutory authority and imposes unrealistic staffing requirements.

The final mandate demands a minimum of 3.48 hours per resident per day (HPRD) of total staffing, with specific allocations for registered nurses (RN) and nurse aides. The allocations call for significant HPRD of direct RN care, and direct nurse aide care, and require the presence of an RN in all facilities at all times. Nursing home operators around the country claim that these requirements are unattainable, unsustainable, and unlawful; they could lead to widespread closures that will put the country’s most vulnerable population at risk.

Partnering with Texas nursing home industry leaders was a fitting move by AHCA as more than two-thirds of Texas facilities cannot meet any of the new requirements and suffer from a nursing shortage that is not expected to abate. The lawsuit emphasizes that, “Texas simply does not have enough RNs and NAs to sustain these massive increases. On the other hand, Texas has a relatively high proportion of licensed vocational nurses (“LVNs”) but the Final Rule largely ignores their important contributions to resident care.”

LeadingAge, with a membership spanning more than 41 states, represents the aging services continuum, including assisted living, affordable housing, and nursing homes. Katie Smith Sloan, president and CEO of LeadingAge, was vociferous in LeadingAge’s stance on the mandate. “The entire profession is completely united against this rule,” she said in a statement. LeadingAge voiced its opposition to the proposed mandate back in 2022, at the outset of Biden’s administration, and now joins the legal battle against its implementation, claiming that, “it does not acknowledge the interdependence of funding, care, staffing, and quality.”

At inception, the new mandate triggered strong opposition from industry leaders and lawmakers. Industry leaders claim the rural areas will take a harder hit than urban areas. Rural facilities are grappling with an unprecedented and acute shortage of registered nurses (RNs), rising inflation, and insufficient reimbursement. Additionally, both Republican and Democratic Congressmen joined in protest of the mandate and threw their support behind the Protecting Rural Seniors’ Access to Care Act (H.R. 5796) which would have effectively suspended the proposal. Ultimately, the staffing mandate was finalized before the House of Representatives took it up.

On the other side of the courtroom, the Centers for Medicare & Medicaid Services’ (CMS) officials maintain that facilities will be able to comply with the mandate because the three phase plan will “allow all facilities the time needed to prepare and comply with the new requirements specifically to recruit, retain, and hire nurse staff as needed.” The lawsuit counters this assertion stating that a delay in deadlines will do nothing to fix the underlying problem.

“To be clear, all agree that nursing homes need an adequate supply of well-trained staff,” the lawsuit states. “But imposing a nationwide, multi-billion-dollar, unfunded mandate at a time when nursing homes are already struggling with staffing shortages and financial constraints will only make the situation worse.”

In conversations with our healthcare clients, the consensus that seems to be forming is that the new staffing mandate’s attempt to address healthcare staffing issues is simply not feasible. The mandate only exacerbates the post-Covid, turbulent environment of the healthcare industry. It is most likely that the legal assault against the mandate has only just begun as nursing home owners and healthcare companies turn to the courts to mitigate the effects of the mandate and to strongarm CMS into drafting a more equitable ruling. How the mandate will ultimately be implemented, which of its components may be reversed, and what adjustments and policy updates will arise, is yet to be seen. Stay ready for updates as the situation evolves.

This material has been prepared for informational purposes only, and is not intended to provide or be relied upon for legal or tax advice. If you have any specific legal or tax questions regarding this content or related issues, please consult with your professional legal or tax advisor.

Taking Back the Keys

While bankruptcies are widely publicized and must follow the established governing codes, there is much more privacy and procedural flexibility when it comes to receiverships. And as we see more portfolios struggling in the current environment of higher interest rates, it’s critical to understand what receivership is and more importantly what it means for you.

Whereas bankruptcy is a method used by debtors to protect themselves from collection; receivership is a remedy that creditors employ to preserve interest upon a breach of contract i.e loan default. Once a breach has occurred, and the parties are unable to come to an agreement otherwise, the creditor will submit a claim to seek receivership in their state court. While a creditor also has the authority to file for involuntary bankruptcy, the receivership process is timelier, less expensive and more importantly, allows the creditor to nominate a receiver of their choice, albeit with the court’s ultimate approval. All these factors are crucial in accomplishing the lender’s goal of restoring their asset’s value.

The responsibilities, rights and compensation of the receiver are subject to the discretion of the court and not bound by strict procedures as seen in bankruptcies. Once finalized, the appointed receiver assumes complete management of the distressed company, controlling all its financial and operating functions. Depending on the litigation proceedings, as the business stabilizes, the lender will look to return the property to the debtor or transition the asset to a new permanent operator. While the company retains its principals in the interim, their authority and insight is limited, to their detriment. Should the business return to profitability or be sold for a gain, they will ultimately be responsible for any taxable income without the ability to proactively tax plan.

Courts view receivership as a drastic step and will encourage the lender and borrower to come to an equitable agreement instead. Should a portion of the debt be forgiven as part of such an agreement, this may result “cancellation of debt” income reported by the borrower. The additional tax liability can be a crushing blow for an already struggling taxpayer.

The two most popular exclusions under Code Section108 are to demonstrate that the company is insolvent or, more commonly, utilizing the ‘qualified real property business indebtedness exclusion.’ This exclusion can apply when real property that secures a debt is held for use in a trade or business and not primarily held for sale. The downside of utilizing this exclusion is that the taxpayer must reduce the tax basis of its depreciable real property by the amount of income he is aiming to exclude; resulting in a decrease in depreciation expense. While this is a worthy trade-off in the short term and can provide necessary breathing room, there are long-term ramifications the taxpayer needs to be aware of. A deteriorated tax basis translates into a higher capital gain should the property eventually be sold. All said, diligent tax compliance and strategic planning are essential to minimize adverse tax consequences during receivership.

While receivership might be perceived as a company’s death knell, it can also present unique opportunities for the company itself, as well as for entrepreneurs and other industry players. Economist Joseph Schumpeter introduced the economic principle of “creative destruction,” which describes how failures or disruptions in income for one entity or sector can create success for others. An entity that enters receivership has the chance to recover, redevelop and thrive. If it does not, others will take full advantage. Those looking to quickly repay creditors present savvy entrepreneurs with an opportunity to acquire assets that can significantly appreciate in value, at discounted prices, and under favorable terms. In business, there are always winners and losers, but opportunities are ever-present. Recognize them and position yourself as a winner.

This material has been prepared for informational purposes only, and is not intended to provide or be relied upon for legal or tax advice. If you have any specific legal or tax questions regarding this content or related issues, please consult with your professional legal or tax advisor.

The ESG Concept – Hype or Value?

The usual question posed by business owners and their leadership teams when they meet to discuss strategic planning is something along the lines of, “How can we safely grow our company to reach the next level of success?” While that is certainly a good launching point, there are other basics to consider. One of them is the environmental, social and governance (ESG) concept.

3 critical components of ESG

ESG generally refers to how companies handle three critical activities:

• Environmental practices. This includes the use of energy, production of waste and consumption of resources.

• Social practices. This includes fair labor practices; worker health and safety; diversity, equity and inclusion. It’s all about a company’s relationships with people, institutions and the community.

• Governance practices. This refers to business ethics, integrity, openness, transparency, legal compliance, executive compensation, cybersecurity, and product or service quality and safety.

Missteps or miscommunications in these areas can spell disaster for a company if it draws public scrutiny or raises compliance issues with regulatory agencies; while integrating robust ESG practices into a company’s strategic planning and daily operations addresses this possible danger and offers many potential advantages.

Benefits

Strong ESG practices could lead to stronger financial performance and offers the following benefits:

• Higher sales. Many customers — particularly younger ones — consider ESG when making purchasing decisions. Some may even be willing to pay more for products or services from businesses that declare their ESG policies.

• Reduced costs. A focus on sustainability can help companies reduce their energy consumption, streamline their supply chains, eliminate waste and operate more efficiently. Conversely, bad publicity associated with government intervention, discrimination or harassment claims, can be costly and damaging.

• Improved access to capital. Clear and demonstrable ESG practices can provide growing companies with access to low-cost capital. Some investors consider a company’s ESG when making additions to their portfolios and may perceive those with ESG initiatives as lower-risk investments.

• More success in hiring and retaining employees. As climate change remains in the public eye, certain job candidates may favor companies that can clearly demonstrate sound environmental practices. Once hired, these employees will likely be more inclined to stay loyal to businesses that are addressing the issue.

Other aspects of ESG also speak to the current concerns and values of workers. Many of today’s employees want more than a paycheck. They expect employers to care for their well-being and protect them from threats such as corruption, unethical behavior and cybercriminals. Comprehensive ESG practices may reassure such employees and keep them close.

Your choice

The importance of ESG practices is not universally agreed upon in the business world. Some approach ESG formally and diligently, while others slide through potential issues. ESG practices are unique to each business and are subject to a company’s leadership team’s judgement. Nonetheless, as a business engages in strategic planning, taking time to consider the impact of ESG-related practices is time well spent. Its potential benefits can only add value in the long run.

This material has been prepared for informational purposes only, and is not intended to provide or be relied upon for legal or tax advice. If you have any specific legal or tax questions regarding this content or related issues, please consult with your professional legal or tax advisor.

Reasons to Buy

When it comes to investment discussions, it often seems as if the “bearish” voices have the upper hand. They sound smarter, more cautious, and more in tune with potential risks. It’s easy to feel that by dismissing their concerns, you look like you’re ignoring the data.

The same negative tone is also prevalent in financial media reporting. For example, the first two headlines that popped up in my search for this article were: “Nvidia’s Ascent to Most Valuable Company Echoes Dot-Com Boom” and “Megacap Stocks Are Extremely Overbought and Could Be Due for a Near-Term Pullback.” The news tends to be painted with a broad, negative brush – always highlighting the next big worry.

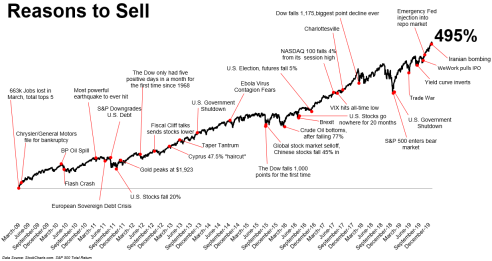

Financial blogger Michael Batnick has an insightful chart he calls, “Reasons to Sell.” The chart plots major news stories that have pushed the market down, alongside the S&P 500. It is fascinating that, while these stories did cause the market to drop for a week, or even a few months, they appear as only blips on the long-term chart. This demonstrates a crucial point: the market tends to recover from short-term shocks and continues its upward trajectory over the long haul.

Negative new stories that yell “Sell!” are ever present, but if you were to attempt to create a chart titled “Reasons to Buy,” the news stories in this category would be few and far between. The steady, long-term belief in the American economy, and its robust ability to rebound (potentially titled “Belief in Human Innovation”), rarely makes headlines. Yet, this enduring strength is the true reason to ‘Buy’.”

Believing that the economy will continue to grow over time may not be a strong counterargument when faced with short-term crises, but for long-term optimists, it means that the timing is always right. This thought is rooted in the concept of economic resilience and human ingenuity. The economy, particularly the American economy, has shown a remarkable ability to recover from downturns, and to innovate and grow. From the Great Depression to the 2008 financial crisis, every major economic setback has been followed by periods of significant growth and innovation.

The “bearish” team may sound more convincing and more focused on risks, but remember that while the market might dip due to legitimate concerns, history shows it tends to bounce back. Maintaining a long-term perspective, and faith in the economy’s growth and in human innovation, can provide a solid foundation for your investment decisions. Investing is not about timing the market; it’s about time in the market. The longer you stay invested, the more you benefit from the economy’s natural growth and the compounding effect of your investments.

While it’s crucial to be aware of risks and to stay informed, it’s equally important to maintain a balanced view. The negative headlines will always be there, but so will the underlying strength and potential of the economy. Trusting in long-term growth and human innovation can help you stay focused on your financial goals, even when the market feels uncertain.

This material has been prepared for informational purposes only, and is not intended to provide or be relied upon for legal or tax advice. If you have any specific legal or tax questions regarding this content or related issues, please consult with your professional legal or tax advisor.

The IRS Grapples with Fraud, Ineligibility, and Processing Backlog. Will We Ever get Our ERC Money?

Back in September of 2023, the IRS declared a moratorium on the processing of new ERC claims, declaring that a substantial portion of the new claims were ineligible and were a product of clueless businesses lured in by promises from aggressive promoters and ‘ERC mills’. Aggressive promotion campaigns by ERC mills instigated a surge of problematic claims, ultimately obstructing IRS’ processing of legitimate claims for deserving businesses. Fast forward to June 2024 and, after coming under pressure from Congress, the IRS has announced that, in an attempt to crawl through the enmired, fraud-ridden ERC program, it will step up its processing and payments of older ERC claims.

Beleaguered IRS Commissioner Danny Werfel clarified that, “We decided to keep the post-September moratorium in place because we continue to be deeply concerned about the substantial number of claims coming in so long after the pandemic. We worry that ending the moratorium might trigger a renewed marketing push by aggressive promoters that could lead to a new round of improper claims. That would be a bad result to taxpayers and tax administration. By continuing the moratorium, we will use this time to consult with Congress and seek additional help from them on the ERC program. Based on what we are seeing, we believe closing the ERC program down to additional applicants would be the right thing to do.”

Werfel says that the IRS continues to be deluged by 17,000 new claims a week, despite the moratorium, and its inventory of claims stands at 1.4 million. According to the law, businesses can still apply for the credit until April 15, 2025, despite the fact that the pandemic is history. The IRS anticipates that tens of thousands of improper high-risk claims for the ERC will be denied. It conducted a review to assess a group of over 1 million ERC claims representing more than $86 billion filed and found that 10% to 20% of claims fell into the highest-risk group, with clear signs of ineligibility or possible fraud. Another 60% to 70% of the claims showed, “an unacceptable level of risk” which will draw extra analysis and scrutiny from the IRS.

Red flags tagging a claim as high risk are those that declare too many employees and wrong ERC calculations, claims based on a supply chain disruption, businesses that claim the ERC for too much of a tax period, or claims from businesses that did not pay wages or did not exist during the eligibility period. Claiming the ERC for partial shutdowns, where a segment of a business was partially shutdown, is also suspect.

Werfel assures taxpayers that the situation is not completely bleak. “For those with legitimate claims, this review helps the IRS with a path forward, and we’re taking action to help. Our review showed between 10% and 20% of the ERC claims show a low risk of red flags. So, for those with no eligibility warning signs, and received before last September, the IRS will begin judiciously processing more of these claims.” The IRS will work on a first-in-first-out basis, with older claims addressed first. It will not process claims that were submitted after Sept. 14, 2023, post-moratorium. Werfel advises taxpayers to lay low and wait for the IRS to sort things out instead of inundating the IRS toll-free line or contacting their accounting professionals to try to speed up the payment process.

While Werfel’s team sorts out its processing issues, the IRS Criminal Investigation unit is hard at work. It has already initiated 450 criminal cases of potentially fraudulent claims totaling a dollar value of almost $7 billion. Of these cases, 36 have resulted in federal charges. At the same time, the IRS has thousands of audits in the pipeline. “So, the bottom line for us on ERC is that we’re continuing to work on many different angles.” Werfel says. “And today’s announcement illustrates that we have a slow but steady path forward to help small businesses with no red flags on their claims, while denying clearly incorrect claims to continuing your work on those claims with question marks.”

This material has been prepared for informational purposes only, and is not intended to provide or be relied upon for legal or tax advice. If you have any specific legal or tax questions regarding this content or related issues, please consult with your professional legal or tax advisor.